Use our revocable living trust form to transfer your estate and other assets to your heirs easily and quickly, avoiding court processes.

Updated July 15, 2024

Written by Sara Hostelley | Reviewed by Susan Chai, Esq.

A revocable living trust form is a document that creates a legal entity (called a trust) to hold assets like real estate, money, and valuables.

The trust is designed to manage assets during your lifetime and organize how your assets will be distributed in the event of your death.

Create a legal entity to hold assets like real estate, money, and valuables.

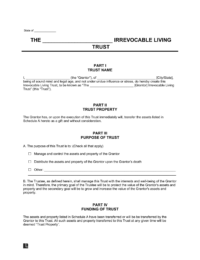

Establishes the terms and conditions of an irrevocable trust.

A revocable living trust (or a revocable inter-vivos trust) provides flexibility for the grantor to manage their assets during their lifetime. They can change or revoke it at any point while they’re alive.

Please note: This document is tied to the grantor’s social security number, so any income the trust generates needs to be filed with the grantor’s taxes.

In many states, this document is a standard tool for protecting property and assets from various life circumstances. Upon the grantor’s death, assets held in the living trust bypass probate, which can be lengthy and costly. As a result, the assets are distributed according to the grantor’s wishes.

For a living trust, you transfer ownership of assets to the trust during your lifetime. This process differs from a testamentary trust, which you can create as part of a last will. Furthermore, a last will only takes effect after the grantor’s death. [1]

Consider why you want to set up a revocable living trust. You may want to provide for your beneficiaries, manage your assets, or start the estate planning process.

Talk to an attorney about your circumstances. They can offer advice and tailor it to your specific situation. They can also ensure that you correctly set up your trust per state laws.

Most states have adopted some form of the Uniform Trust Code to govern the creation and interpretation of revocable living trusts. While it’s advisable to hire an attorney, you can familiarize yourself with the state laws for living trusts below:

Decide which assets you’d like to place in your trust. While a trust can be a beneficial way to manage assets, you may decide against placing certain assets in a trust.

For example, placing retirement accounts, such as 401(k)s and IRAs, into a trust may result in negative tax consequences. Furthermore, you may refrain from putting personal items into a trust, as handling their transfer through a more informal arrangement may be simpler.

Select a trustee to manage your trust. When you first create the trust, you can name yourself the trustee. This way, you won’t give up control too early or easily. However, you can appoint another trusted individual as the trustee from the beginning.

You can also select a successor trustee who will take over the management responsibilities if you (or your appointed primary trustee) pass away or become incapacitated.

Fill out your trust form, including key details on how the trustee should manage the assets. You should also specify the procedures for asset distribution for when you’re alive and after you pass away.

Finalize the trust agreement by making your trust the owner of your assets. You may have to change the title of an asset (for real estate) or modify the beneficiary designation of an asset to deem the trust as the owner.

Acquire the grantor’s and trustee’s signatures. For added authenticity, have both parties sign before a notary public. Please review your state’s laws to determine if your jurisdiction requires witnesses to be present as well.

Regularly review and update your revocable trust. You should especially do so after major life events, such as a job loss, the birth of a new child, a divorce, or a marriage.

The main difference between a revocable and irrevocable living trust is the degree of control and ownership the grantor has over the trust once they create it.

A revocable living trust can be modified or terminated by the grantor at any time as long as the grantor is mentally competent at the time of the decision. The assets in the trust are the grantor’s property, and such property must be filed with their income taxes. Conversely, an irrevocable living trust cannot be altered or revoked by the grantor without the beneficiaries’ permission.

Here’s a table summarizing the differences between these two trusts:

| Question | Revocable Living Trust | Irrevocable Living Trust |

|---|---|---|

| Can I change or revoke it after creating it? | Yes. The grantor can amend, modify, or revoke the trust while they're alive. | No. Once the grantor executes this document, it's very difficult for them to make changes or revoke it. |

| Does the grantor maintain control over their assets? | Usually, yes. The grantor is often the initial trustee. | Usually, no. The grantor typically gives up control once they transfer assets into the trust. |

| Are the assets safeguarded from creditors? | No. Assets remain subject to the grantor's creditors because the grantor can revoke the trust. | Possibly. The assets may be safeguarded from creditors, depending on the circumstances and local laws. |

| Does it avoid probate? | Yes. | Yes. |

| Does it provide tax benefits? | It doesn't provide any significant tax benefits because it's subject to tax under the grantor's estate. | It may provide potential estate tax savings, income tax planning benefits, and asset protection from estate taxes. |

| Is it more complex to create and manage? | It's generally less complex because it offers fewer restrictions and more flexibility. | It's generally more complex because it offers less flexibility and has stricter legal requirements. |

| Is it part of the grantor's taxable state? | Yes. | No. |

A trust is an essential estate planning document that can be created as an alternative to or in conjunction with a last will and testament (which does not protect your assets from probate).

For most people, we recommend creating both documents. Realistically, not everything you own can be transferred into a trust during your lifetime, so some assets will be transferred according to your state’s intestate succession laws if you don’t have a will. Additionally, a last will provides specific functions that trusts don’t, such as naming a guardian for minor children.

Here’s a summary of the key differences between these documents:

| Question | Revocable Living Trust | Last Will and Testament |

|---|---|---|

| Does it avoid probate? | Yes. It may be quicker and cheaper to distribute assets to beneficiaries using a revocable living trust. | No. Assets issued via a will must go through the time- and cost-extensive process of probate. |

| Is it private? | Yes. It typically remains private and doesn't become part of the public record. | No. Anyone can see the contents of a will because it becomes a public document once it enters probate. |

| Is it more complex to set up? | It's generally more complex to set up. | It's generally simpler to create. |

| Does it allow for the management of assets during incapacity? | Yes. The trustee can manage the grantor's assets if the grantor becomes incapacitated. | No. A will only becomes effective once the grantor passes away. |

| Can I amend it easily? | Yes. | Yes. You can use a codicil to will to do so. |

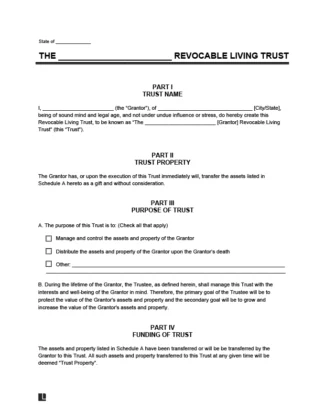

Follow the steps below to complete your trust document:

Fill out the name and address of the person (or people) putting property into the trust.

The most common reason for creating a trust is to manage and distribute your assets, but you can include any other lawful reason you choose.

Indicate who will serve as the initial trustee(s) and the successor trustee(s). Often, the grantor will choose themself as the initial trustee so they can continue to manage the trust assets during their lifetime.

Decide who will receive assets from your trust, whether as a particular gift or as a percentage of the trust. Beneficiaries can be either people or organizations (such as a charity).

In most states, you must acknowledge the trust document before a notary public to ensure your signature is valid. Check your state’s requirements if you’re unsure.